David Carrington explains why arts organisations seeking commercial support could learn important lessons from the way Tate conducts itself as revealed through the recent BP sponsorship Freedom of Information case.

David is an independent consultant and governance adviser. This article is part of ‘Mind the Gap: expert evaluations of Tate’s ethical decision-making over BP‘. For more expert comment and a summary briefing, see Mind the Gap. To view the original documents from Tate’s Ethics Committee (pdf), click here. First published on Arts Professional.

In September 2014, the Information Tribunal forced Tate to reveal information about its sponsorship deal with oil company BP, following three years of Freedom of Information appeals by arts and campaigning groups Platform and Request Initiative. The groups’ appeal asserted that Tate’s refusal to disclose certain sponsorship information was against the public interest, namely growing concern around oil companies’ environmental and human rights impacts, including climate change.

In September 2014, the Information Tribunal forced Tate to reveal information about its sponsorship deal with oil company BP, following three years of Freedom of Information appeals by arts and campaigning groups Platform and Request Initiative. The groups’ appeal asserted that Tate’s refusal to disclose certain sponsorship information was against the public interest, namely growing concern around oil companies’ environmental and human rights impacts, including climate change.

The two specific issues under appeal were Tate’s historic BP sponsorship figures 1990-2006, and Tate’s heavy redactions of its Ethics Committee meeting minutes in 2010 and 2011 where the Committee would have deliberated on whether to renew its sponsorship relationship with BP. This was in the context of BP’s 2010 Deepwater Horizon disaster.

Tate’s refusal to disclose the information through the original Freedom of Information request not only fuelled more media opportunities for those concerned by the oil sponsorship, but must also have been very costly to Tate in terms of time and lawyers’ fees. Furthermore, by initially refusing to disclose their ethical deliberations about renewing the BP relationship in 2011[i], Tate comes across in a less than transparent light. In January 2015, the Tribunal judges issued their ruling that, in the public interest, Tate must disclose the BP sponsorship figures 1990 – 2006, and that a great deal more of the redacted Ethics Committee meeting minutes – specifically its ethical deliberations on BP as suitable sponsor – must be unredacted[ii].

So, what are the factors that should have been considered when Tate was assessing the appropriateness of BP as a sponsor? Could a more rigorous process have operated? I was asked to consider the material now in the public domain as a result of the Tribunal ruling and to comment on what these reveal about the governance approach adopted by Tate in 2010 in relation to the renewal of BP sponsorship. My comments relate not only to the past as the five-year deal comes up for renewal in 2016. Tate is deliberating right now about the future of its BP sponsorship.

Gift or Sponsorship?

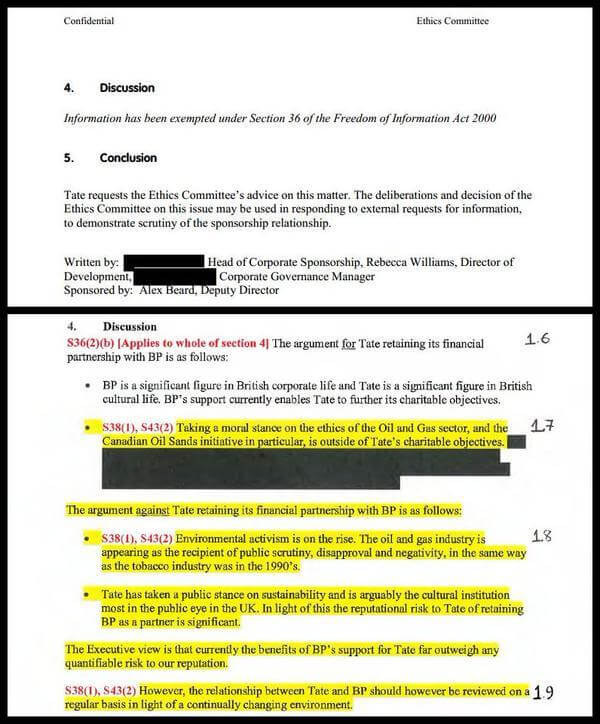

I found a surprising amount of inconsistency in meeting minutes and supporting documents about whether the financial support from BP were charitable donations or corporate sponsorship. The funding was referred to in different papers using both terms. This is not just an issue of semantics as the differences between these two forms of funding are significant, not least in expectations and perceptions of them, both within the two organisations and to external observers. Some of the comments made, for example, in the minutes of the Ethics Committee suggest that BP’s support was viewed as if it was a series of charitable donations whereas it is clear that it was commercial sponsorship, contributions made not as philanthropic gifts but as part of the profile-building Corporate Social Responsibility and marketing strategy of the company. There are several references in the May 2010 Ethics Committee minutes where it seems to be suggested that a charity such as Tate would be acting outside of its charitable purposes if the trustees chose to refuse an offer of funds – “taking a moral stance on the ethics of the Oil and Gas sector, and the Canadian Oil Sands initiative in particular, is outside of Tate’s charitable objectives.” Such a position may apply in the case of a donation (though reputational risk could still influence the trustees’ decision), but does not seem to me to apply to whether a charity should seek (or accept) commercial sponsorship; the latter is a contract within which the charity provides services and marketing opportunities in return for payment – it is not a philanthropic donation.

For any discussion of the merits or otherwise of proposed or renewal of support from a commercial entity, the staff and trustees of a charity must all be clear as to the nature, terms and acceptability of the proposed funding or misunderstandings and confusion are likely, indeed inevitable.

‘Subject to Confidentiality Agreement’

Tate refers regularly throughout the papers to its confidentiality agreement with BP – this is used to justify not disclosing the terms or amounts of the funds in the sponsorship deal. Given that the use of the funds to support specific Tate activities has been given considerable prominence by both Tate and BP, it is hard to see what can be ‘confidential’ about the sponsorship agreement, except a wish by both organisations to conceal the actual amount of funding involved in the sponsorship. The sponsorship agreement is not the product of some highly competitive tendering process or a commercial contract full of trade secrets or intellectual property issues. Why then is there any element requiring confidentiality? Surely it is in the interest of both organisations to be fully transparent about the relationship and to celebrate its achievements and mutual benefits, especially as it has been maintained for so long. It may be that in 1990, when the BP/Tate relationship was first established, attitudes towards transparency were different from those that prevail today – but that does not mean that they should have been maintained uncritically as each period of sponsorship was negotiated.

Even the Cabinet Office has recently asserted that an “overarching transparency principle” should apply in relation to contracts with public service providers and that there “should be a presumption in favour of disclosing information….commercial confidentiality being the exception rather than the rule.”[iii] The preamble to the Government’s transparency principles, though focused on public service delivery contracts, has, with only a few changes to the text, a direct relevance to commercial sponsorship of arts organisations: “Transparency and accountability of public service delivery is key as it builds the public’s trust and confidence in public services, enables citizens to see how taxpayers money is being spent and enables the performance of public services to be independently scrutinised.”

In the case of the Tate/BP commercial sponsorship agreement, it is hard to see how the relationship would have been harmed or undermined if such an attitude to transparency had been adopted. In considering the case for renewal of the relationship – in 2010 certainly, but probably some years earlier too – Tate could (and, to my mind, should) have proposed the adoption of a standard of transparency no less than that which the Cabinet Office sets out in its principles; and should have resisted any imposition by BP of the continuation of whatever were the terms of the confidentiality agreement agreed for previous periods of the sponsorship deal. If that had been done, as we can now see, a huge amount of executive, trustee, and legal time and expense dealing with the FoI challenge could have been avoided.

Sustainability

At a time when Tate was adopting a ‘vision’ to “become a leader in museum sustainability practice and to influence the entire sector towards more sustainable environmental practice”[iv], there was clearly the potential for tension and controversy about seeking a renewed sponsorship deal with a company primarily engaged in oil and gas extraction – the more so in the same year as BP was at the centre of the Deepwater Horizon disaster in the Gulf of Mexico. To an outsider, it seems curious that, when adopting the new sustainability vision, Tate did not simultaneously examine whether it could create opportunities to reinforce the credibility of the new policy by seeking out new sponsorship arrangements with companies that are wholly engaged in renewable or other environmentally sustainable activity. Not to do so – and, at the same time, to seek the renewal of a high profile association with BP – exposes the governance of Tate at least to reputational scepticism about its commitment to the sustainability vision. I could not find in the papers that I have read any discussion at Board or Committee level as to what options might be available to match the adoption of the sustainability vision with the development of a complementary fund-raising strategy and initiatives to seek new corporate partnerships with companies wholly committed to sustainability practices throughout all of their work. It does seem to me that there has been a lack of a ‘joined up’ governance about these issues within Tate – with what now must be perceived as expensive and counterproductive consequences.

What if BP was being considered as a new sponsor today?

The minutes and papers that I have seen emphasise strongly the long-term nature of the relationship between BP and Tate. This is indeed significant and worthy of celebration – but times and attitudes change. Papers prepared by the Executive for the Ethics Committee acknowledge that consideration by Tate of the future relationship with BP should be reviewed in the “light of a continually changing environment” but there is no indication that staff or trustees stepped back from the existing relationship with BP and asked themselves what stance they would take if in 2010, for the first time, Tate had received an offer of corporate sponsorship from BP or it was proposed that such sponsorship be sought. Rather than focusing so much on the longevity of the past sponsorship deal, it might have been better governance to assess the case for starting a relationship with BP in an era when issues about and attitudes to oil and gas extraction and climate change are so very different than when the original sponsorship deal with BP was negotiated; and at a time when Tate was seeking to present itself as a leader on sustainability and to influence the entire arts sector towards more sustainable practice.

David Carrington

April 2015

[i] ) The announcement of a 5-year renewal of BP’s sponsorship of Tate, Royal Opera House, British Museum and National Portrait Gallery was made in December.

[ii] ) https://www.theguardian.com/artanddesign/2015/jan/26/tate-reveal-bp-sponsorship-150000-330000-platform-information-tribunal

[iii] ) https://www.gov.uk/government/publications/transparency-of-suppliers-and-government-to-the-public

[iv] ) https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/247630/0376.pdf